Search

Europe’s Private Water Utilities: Company Profiles, Rankings, & Trends, 2016

Europe's top 15 consolidated private water utilities serve over 147 million of people in 11 countries, covering just under 30% of total population.Canada Municipal Water Infrastructure: Utility Strategies & CAPEX Forecasts, 2016-2025

Canada’s municipal utilities are on track to spend C$72 billion (or C$2,500 bill per person) on water infrastructure over the next decadeSmart Water Meters in Europe: Utility Strategies Drive Adoption, 2016-2020

Market insight analyzing utility strategies to drive smart water meter adoption. Available for purchase and immediate download

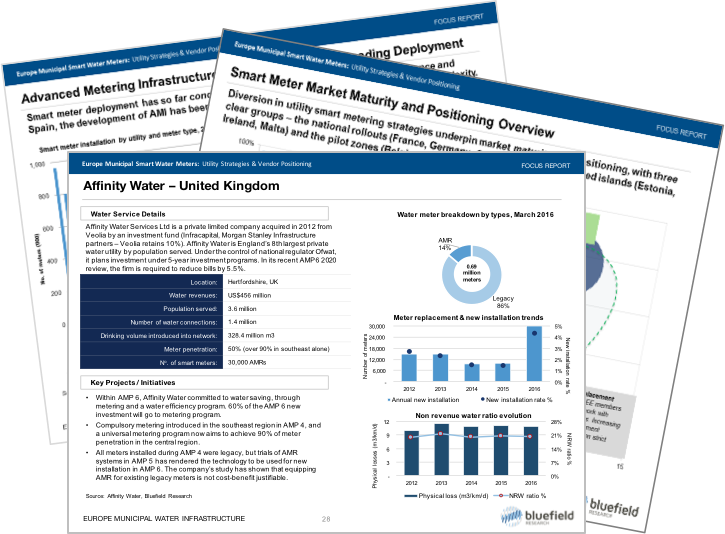

European water utilities are deploying new strategies to become more efficient– taking steps to address non-revenue water and leakage management, while improving customer service. Smart meters are a critical first step– allowing utilities to harness the value of “Big Data” to manage unbilled water consumption and rising capital and operating costs.

This new Market Insight from Bluefield is essential for companies evaluating investment needs, outlook, opportunities, and trends in smart water across Europe. Topics covered include:

- Market Drivers & Inhibitors for Smart Meter Deployment

- Utility and Vendor Metering Strategies

- Profiles of the 40 largest municipal utilities

- Profiles of the leading smart water meter vendors

Follow this link to access the Table of Contents

Click here for sample slides

Key questions addressed:

- What is the size of the European smart water meter market and what is the addressable opportunity?

- Where are metering rollouts expected to take place by country and by utility?

- What are the most successful utility strategies for driving the adoption of smart water metering?

- Which vendors are best-positioned in terms of utility wallet share and value chain?

- How will EU directives and national water policies impact smart meter spend over the next decade?

Special pricing available this week. Contact us to learn more.

KKR Rebalances Water Portfolio

US investment firm Kohlberg Kravis Roberts & Co. sold its remaining 23.85% share of wastewater treatment firm CITIC United Envirotech Limited...U.S. EPA Industrial Consent Decrees: Judicial Consent Decree Trends and Planned Investment

The EPA has issued 95 consent decrees to industrial violators of the Clean Water Act, totaling more than US$6.4 billion in civil penalties. This Data Insight...Municipal Utility Districts in Texas: Emerging Drivers, Trends, & Opportunities

The Municipal Utility District (MUD) market for water infrastructure services is highly concentrated in Texas - Bluefield analyzes market drivers and inhibitorsVendors Zero in on UK Leakage Management

A set of deals in the past month has underlined the attractiveness of the UK’s leakage management market for technology solutions providers.The Changing Topography for Private Participation in Water // NAWC

Private participation in U.S. municipal water markets is poised for expansion. More than 19 deals totaling US$384 million (completed and pending) were put on the books for the first half of this year. This presentation, first given by Bluefield President Reese Tisdale at the NAWC summit in San Diego, analyzes the changing topography for private participation in water markets. This presentation looks at:

- The Changing US Municipal Utility Landscape

- Key Market Drivers for Private Investment

- Evolving Private Water Landscape

These and other findings are from Bluefield’s new report, U.S. Private Water Utilities: Market Trends, Strategies & Opportunities, 2016. This report provides strategic analysis of the top 25 investor-owned utilities, identifies key trends for private participation, and evaluates new opportunities for private players across state markets.